Speak the Home Buying Language

- Jovan Brown

- Jun 23, 2021

- 2 min read

Updated: Oct 8, 2021

The best time to buy a house is when you’re ready, but buying a home can be intimidating if you are not familiar with the most common phrases used during the process.

Use the below list to help yourself get acquainted with the terms. You’ll be surprised at how much easier the process will be if you’re up to speed with the lingo.

“Real estate investing, even on a very small scale, remains a tried and true means of nuilding an individual's cash flow and wealth.”

Appraisal

You’ll hear your real estate agent talk about this once you’re in contract. An appraiser will have to come through the house to provide an unbiased estimate of what the house is worth.

Closing Costs

You’ve made it! It’s closing time. But with the closing, comes costs.

By definition, closings costs are all transaction charges that home buyers or sellers need to pay at the close of escrow when the property is transferred. Typically, closings costs range from 2 to 5 percent of the purchase price.

Contingency

“We will only move forward with the sale as long as x, y, and z happen.”

A contingency can be placed by either the buyer or the seller. It’s a provision in the contract stating that some or all of the terms of the contract will be altered or voided by the occurrence of a specific event.

Escrow

You’ll hear this term once you put an offer on a house. Escrow is defined as the holding of funds by a neutral third party prior to closing.

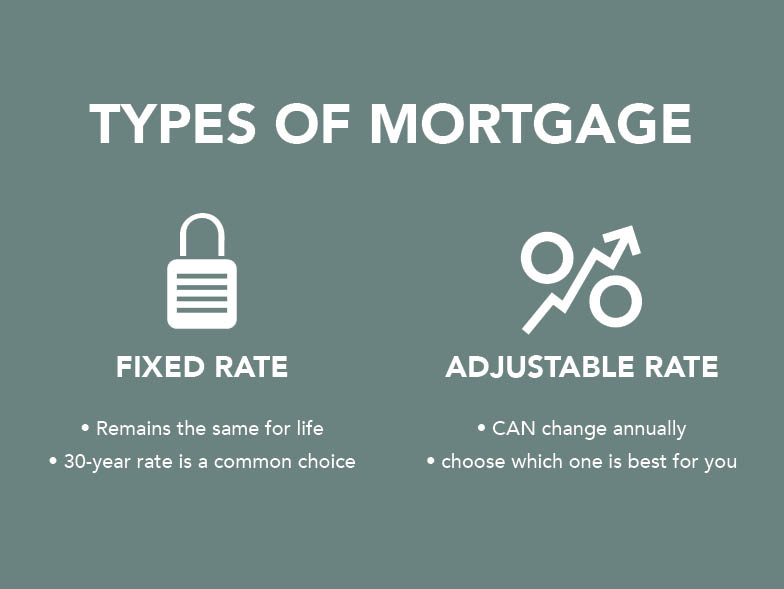

Fixed-Rate Mortgage

Mortgage rates are discussed when you meet with a broker. A fixed-rate mortgage is a loan that has an interest rate which will remain the same for the life of the loan. The most popular is the 30-year loan because it makes your payments the lowest.

Adjustable-Rate Mortgage

On the contrary, the interest rate on an adjustable-rate mortgage can change from year to year. You’ll want to discuss the pros and cons of both a fixed and adjustable mortgage with your broker.

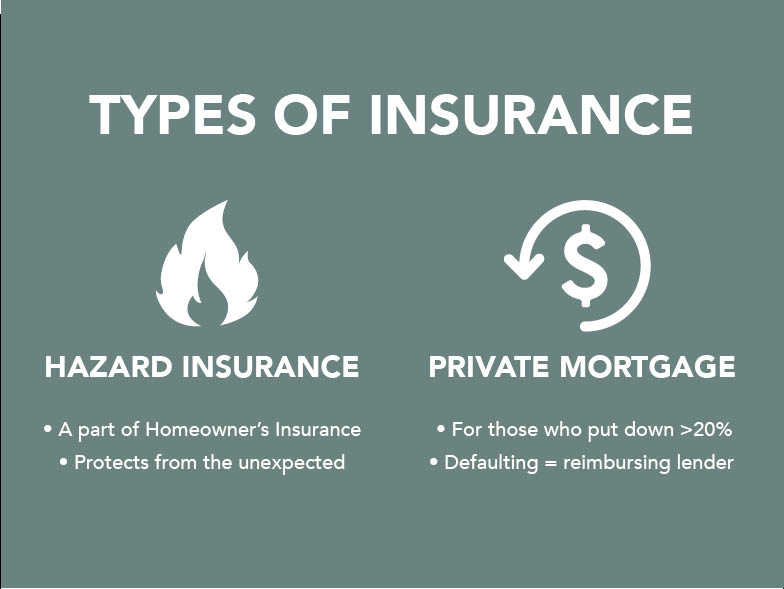

Hazard Insurance

Unfortunately, accidents happen. Hazard insurance is a part of the homeowner’s insurance bundle that’s required when purchasing a home. It protects against physical damage to a property caused by unexpected events such as fires, storms, and vandalism.

Private Mortgage Insurance (PMI)

The good news is that you don’t need to put 20 percent down to purchase a home. However, if you choose to put less than 20 percent down, you’re required to purchase private mortgage insurance. PMI is a type of insurance that reimburses the lender if you default on the loan.

Title

The keys are yours and so is the title! The title is a fancy wordy for the ownership of real estate.

source: https://www.keepingcurrentmatters.com/blog/

Comments